Illinois law gives eligible family members the right to recover compensation, but settlement outcomes vary enormously. The difference between a fair result and an inadequate one often comes down to evidence quality, damage documentation, negotiation strategy, and whether the family has experienced legal representation.

This guide covers who can file a wrongful death claim in Illinois, how the negotiation process works step by step, what drives settlement value, and the mistakes that most commonly cost families money.

TL;DR

- Illinois law sets a deadline of two years from the date of death to file — acting quickly preserves evidence and legal options

- Establish clear liability and document every category of damage before sending any settlement demand

- Never accept the first offer — initial offers are intentionally low and rarely reflect full authorized value

- Settlement value is driven by liability strength, the deceased's earning capacity, number of dependents, and how well non-economic damages are documented

- Credible willingness to go to trial is your most powerful negotiating tool — use it

What Families Should Know Before Negotiating a Wrongful Death Settlement

Who Can File a Wrongful Death Claim in Illinois?

Under Illinois law, a wrongful death claim must be brought by the personal representative of the deceased's estate — an executor named in a will or an administrator appointed by the court. Individual family members cannot file independently.

The damages recovered are distributed to the surviving spouse and next of kin — Illinois law expressly includes adopting parents and adopted children in that definition. The trial court allocates settlement proceeds based on each beneficiary's degree of financial dependency on the deceased.

If no will names an executor, the court appoints an administrator before any negotiation can proceed. Identifying and confirming that representative is the required first step.

Illinois Statute of Limitations

Under 740 ILCS 180/2, Illinois families generally have two years from the date of death to file a wrongful death lawsuit. Miss that deadline and the right to seek compensation is gone entirely.

A few narrow extensions exist:

- Deaths from violent intentional conduct: five-year deadline (or one year after criminal case disposition)

- Beneficiaries under 18: two years after reaching adulthood

Delay also weakens a case on practical grounds. Surveillance footage gets overwritten, witnesses become unreachable, and physical evidence disappears. Acting early protects both the legal right and the evidentiary record.

What Damages Are Available in Illinois Wrongful Death Cases?

Illinois allows two categories of compensable damages:

Economic damages:

- Funeral and burial costs

- Medical bills from the final injury or illness

- Lost future wages, benefits, and retirement contributions

- Loss of household services

Non-economic damages:

- Grief, sorrow, and mental suffering

- Loss of companionship and society

- Loss of guidance for surviving children

Illinois expressly includes grief and mental suffering as recoverable "pecuniary injuries" under the Wrongful Death Act — and following Best v. Taylor Machine Works, there is currently no statutory cap on non-economic damages in these cases. Document emotional and relational losses carefully. With no cap in place, thorough evidence of grief, lost companionship, and disrupted family relationships directly shapes the settlement figure.

How to Negotiate a Wrongful Death Settlement: Step-by-Step

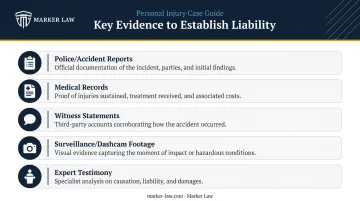

Step 1: Establish Liability with Strong Evidence

No negotiation proceeds without first proving the defendant's negligence caused the death. Ambiguous or incomplete liability evidence gives insurers grounds to deny claims outright or offer a fraction of fair value.

Evidence that establishes liability includes:

- Police or accident investigation reports

- Medical records documenting cause of death

- Witness statements

- Surveillance or dashcam footage

- Expert testimony (accident reconstruction, toxicology, engineering)

The stronger the liability case before the first demand letter goes out, the less room the insurer has to dispute the claim. Jason Marker at Marker Law spent three years on the defense side — he knows what adjusters look for when deciding whether to fight a claim or negotiate seriously.

Step 2: Calculate the Full Scope of Damages Before Negotiating

Rushing into negotiations before all damages are quantified is one of the most costly mistakes families make. Once a settlement is signed and a release is executed, the case cannot be reopened — regardless of what future costs emerge.

For economic damages, gather:

- Pay stubs, tax returns, and employer letters to document income history

- Projections from a forensic economist for future lost earnings (accounting for worklife expectancy, benefits, wage growth, and present-value discounting)

- Documentation of household services the deceased provided

For non-economic damages, build a record with:

- Personal journals and written accounts from family members

- Mental health records documenting grief and psychological impact

- Statements describing the specific relational role the deceased played

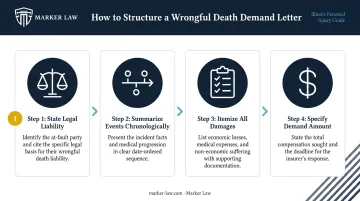

Step 3: Send a Well-Supported Demand Letter

The demand letter formally opens settlement negotiations and sets the anchor for every offer and counteroffer that follows. A well-constructed letter should:

- State the legal basis for liability clearly

- Summarize the events in chronological order

- Itemize all damages with supporting documentation attached

- Specify a demand amount set above the family's minimum acceptable figure

The opening demand creates the negotiating range. A demand letter that arrives with thorough documentation signals to the insurer that the family is organized, prepared, and not going away. Adjusters respond differently when they can see the family is ready to litigate.

Step 4: Counter the Insurance Company's Response Strategically

Expect the insurer's first response to include a low counteroffer, a liability dispute, a request for additional documentation, or some combination of all three. Illinois Insurance Code Section 154.6 identifies as an improper claims practice compelling policyholders to litigate by offering substantially less than amounts ultimately recovered — but this doesn't stop insurers from trying.

Effective counter-negotiation strategies:

- Address each disputed point with specific, documented evidence

- Make moderate concessions rather than large drops that signal desperation

- Never reveal the minimum amount the family will accept

- Maintain a consistent posture that litigation is a real option

Having worked the defense side, Jason Marker has seen the same playbook used repeatedly. The tactics families encounter most often:

- Delays designed to create financial pressure

- Excessive documentation requests meant to slow momentum

- Early settlement pushes before the family understands the full value of the claim

Step 5: Evaluate the Final Offer and Decide Next Steps

Before accepting any offer, run it against these benchmarks:

- Covers all documented economic damages, including projected future losses

- Provides meaningful compensation for non-economic losses like grief and lost companionship

- Reflects the strength of liability evidence and comparable outcomes in the same jurisdiction

Settlement offers certainty and a faster resolution. Trial offers the possibility of a larger award but comes with longer timelines, litigation costs, and outcome risk. This decision should be made with qualified legal counsel who understands both the law and the specific dynamics of the local court system.

Factors That Determine Your Wrongful Death Settlement Value

No two wrongful death cases settle for the same amount. These are the variables that matter most.

Strength and Clarity of Liability Evidence

When fault is clear and well-documented, insurers have limited room to dispute the claim. Contested liability is the most common reason insurers reduce offers sharply.

Cases involving unambiguous negligence — a documented workplace safety violation, a DUI-caused fatality, clear distracted driving evidence — generate stronger negotiating positions than cases where fault is disputed or shared.

The Deceased's Age, Income, and Earning Trajectory

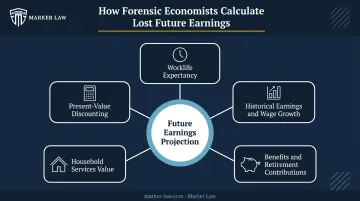

Lost future earnings are typically the largest component of economic damages. Forensic economists project these losses using:

- Worklife expectancy

- Historical earnings and projected wage growth

- Benefits and retirement contributions

- Household services value

- Present-value discounting

Younger victims with established career trajectories tend to generate larger economic damage claims. For retired or elderly victims, non-economic damages carry relatively more weight.

Number and Financial Dependency of Surviving Family Members

Surviving spouses and minor children who relied on the deceased financially represent a direct, quantifiable economic loss. Illinois courts assess each beneficiary's dependency percentage when distributing settlement proceeds.

The composition of the surviving family shapes the claim in distinct ways:

- Minor children carry longer projected dependency periods, increasing compensable economic loss

- Surviving spouses who shared household income represent ongoing financial partnership losses

- Adult children who were financially independent have a weaker economic dependency claim, shifting weight to non-economic damages

Documentation Quality for Non-Economic Damages

Grief, mental suffering, and loss of companionship are recoverable under Illinois law — but they're inherently subjective. The more thoroughly documented they are, the harder they are for insurers to dismiss.

Strong non-economic damage documentation includes:

- Written accounts from family members describing specific losses

- Mental health records showing grief's psychological impact

- Personal journals reflecting the relational role the deceased played

Common Mistakes Families Make When Negotiating Wrongful Death Settlements

Insurance companies negotiate these claims professionally. Families dealing with grief rarely do. These are the mistakes that most reliably reduce or eliminate valid compensation.

- Accepting the first offer — Opening offers test whether the family understands the claim's real value. Accepting before all damages are documented leaves significant compensation on the table.

- Settling before damages are fully tallied — Final medical bills, funeral costs, and long-term income projections often aren't complete in the weeks after death. A signed release permanently closes the case; nothing that surfaces later is recoverable.

- Disclosing the minimum acceptable amount — The moment a family reveals the lowest number they'll take, the insurer anchors there. Adjusters are trained to extract this information and stop negotiating above that floor.

- Negotiating without an attorney — Insurance adjusters handle wrongful death claims as a routine part of their job. Families navigate them once, while grieving. That imbalance consistently produces worse outcomes for unrepresented claimants.

Marker Law handles wrongful death cases on a contingency fee basis — families pay nothing upfront and owe no attorney fees unless compensation is recovered. Jason Marker offers a free initial consultation and brings direct defense-side experience to every case, giving families the same insight into adjuster decision-making that adjusters use against them.

What to Do When Wrongful Death Settlement Negotiations Fail

If negotiations stall or the insurer refuses to offer fair value, filing a lawsuit doesn't mean abandoning settlement — it changes the dynamic. Once litigation begins, the insurer's exposure increases substantially — and that shift in pressure often prompts a genuine reassessment of the claim's value.

Filing a wrongful death lawsuit signals that the family is genuinely prepared to pursue the case to verdict. It also sets in motion several processes that insurers would rather avoid:

- Formal discovery and document production

- Depositions of witnesses and company representatives

- Exchange of expert reports that quantify damages

Many cases that failed to resolve before filing settle during litigation once the full evidence is on the table.

Mediation is commonly used as a middle step. A neutral third-party mediator guides structured negotiation between both sides in a confidential setting. Illinois Supreme Court Rule 99 authorizes judicial circuit mediation programs, and mediation frequently resolves disputes that direct negotiation couldn't — without the cost, delay, and uncertainty of a full jury trial.

Frequently Asked Questions

How much is the average wrongful death settlement?

There is no reliable average. Settlement amounts vary based on the deceased's age and income, the number of financial dependents, liability strength, and the quality of non-economic damage documentation. An attorney can evaluate the specific facts of a case to provide a realistic range.

What should I not say during settlement negotiations?

Never disclose the minimum amount you would accept. Avoid statements that suggest shared responsibility for the death, and don't express financial urgency. Insurance adjusters are trained to exploit all three of these to stop negotiating and anchor the final offer.

How do you successfully negotiate a wrongful death settlement?

Strong negotiations follow a clear sequence:

- Build a solid liability case before making any demand

- Document every damage category thoroughly — economic and non-economic

- Send a well-supported demand above your target amount

- Counter with documentation, not emotion

- Be genuinely prepared to litigate if fair compensation isn't offered

What are signs of a good settlement offer?

A fair offer fully covers documented economic damages, including projected future income losses. It also provides meaningful compensation for non-economic losses like grief and loss of companionship, and aligns with comparable wrongful death outcomes in the same jurisdiction.

How long does a wrongful death settlement take?

Timelines range from several months to several years. Cases with clear liability and thorough initial evidence packages tend to move faster. Disputed liability or complex damages calculations extend the timeline, and cases requiring litigation can take considerably longer.

Do I need a lawyer to negotiate a wrongful death settlement?

Families aren't legally required to hire an attorney, but insurance companies assign trained adjusters to handle these claims routinely. Unrepresented families are at a structural disadvantage. Contingency fee representation costs nothing upfront and typically produces higher net recoveries even after deducting attorney fees.